Thousands of taxpayers face unexpected penalties each year for filing taxes late, making late payments, or even making honest mistakes on their tax returns. In 2023, the IRS assessed over $25.6 billion in additional taxes for late-filed returns and collected $2.8 billion from delinquent tax filings.

The worst part is that most individuals and businesses don’t realize they have options to reduce or eliminate these tax penalties. Whether you forgot to file, underestimated your tax payments, or faced financial hardship, there are available tax penalty relief options that you may be eligible for.

What Are IRS Tax Penalties?

The IRS issues penalties when taxpayers fail to file, fail to pay, or fail to follow federal tax requirements. These penalties can apply to individuals, self-employed taxpayers, and businesses. Many penalties also generate daily compounding interest, which means the balance grows until the underlying tax is fully resolved.

Here are the most common IRS tax penalties:

Failure-to-File Penalty

Charged when you do not file a required tax return by the deadline. This is often the most expensive IRS penalty and increases every month your return remains unfiled.

Failure-to-Pay Penalty

Assessed when you file a return but do not pay the full tax owed. This penalty continues to grow until the balance is paid in full or placed into an approved IRS payment plan.

Failure-to-Deposit Penalty (Payroll Taxes)

Applied to businesses that do not deposit employment taxes on time or in the correct amount. These penalties escalate quickly and can trigger aggressive IRS enforcement if left unresolved.

Accuracy-Related Penalties

Issued when the IRS determines you underreported income, overstated deductions or credits, or were negligent in preparing your return. These penalties are typically 20% of the underpaid tax.

Underpayment of Estimated Tax Penalties (New Addition)

Assessed when you do not pay enough tax throughout the year through withholding or estimated quarterly payments. Common for self-employed taxpayers, gig workers, investors, and anyone with uneven income.

👉 If you are struggling with more IRS tax debt than you can manage, you are not alone. Read our Fast-Track Guide to Tax Debt Relief under the IRS Fresh Start Program for 2026.

The IRS is Forgiving Millions Each Day. You Could Be Next.

First-Time Penalty Abatement (FTA)

You may be in luck if you’ve been hit with a tax penalty for the first time. The First-Time Penalty Abatement (FTA) program allows eligible taxpayers to have their penalties removed—no lengthy explanations or documentation required. It’s one of the easiest ways to get relief, but many taxpayers don’t even realize they qualify.

Who Qualifies for First-Time Penalty Abatement?

To be eligible for FTA, you must meet these three criteria:

- No prior penalties in the past three years (excluding estimated tax penalties).

- All required tax returns are filed, even if filed late.

- Any taxes owed are either paid in full or have a payment plan set up with the IRS.

If you meet these conditions, you can request FTA for failure-to-file, failure-to-pay, or failure-to-deposit penalties on individual or business tax returns.

Which Penalties Can Be Removed?

FTA applies only to three categories of IRS penalties:

- Failure-to-File penalty

- Failure-to-Pay penalty

- Failure-to-Deposit penalty (business payroll taxes)

It does not apply to:

- Accuracy-related penalties

- Underpayment (estimated tax) penalties

- Fraud penalties

- International information return penalties

How to Request FTA

Filing for a First-Time Penalty Abatement is relatively simple. Here’s how:

- Call the IRS at 1-800-829-1040 (individuals) or 1-800-829-4933 (businesses) and ask for penalty relief under FTA.

- Submit Form 843, Claim for Refund and Request for Abatement, if you prefer to request it in writing.

- If the penalty has already been paid, you may be able to get a refund or credit toward future taxes.

Attorney Insight

👉 FTA is a powerful tool, but only if you meet IRS compliance rules. Many taxpayers are denied simply because a missing return or old penalty is still on their transcript. A quick compliance review by a tax attorney can mean the difference between an approval and another IRS denial letter.

Reasonable Cause Penalty Relief

Sometimes, life throws unexpected challenges your way—illness, natural disasters, financial hardships—that make it impossible to meet tax deadlines. The IRS recognizes this and offers Reasonable Cause Penalty Relief for taxpayers who can prove that circumstances beyond their control prevented them from filing or paying on time.

What Qualifies as a Reasonable Cause?

The IRS evaluates requests for Reasonable Cause Relief on a case-by-case basis, but common acceptable reasons include:

- Serious illness, incapacitation, or death of the taxpayer or an immediate family member.

- Natural disasters, fires, or other catastrophic events that prevented timely filing or payment.

- IRS errors or incorrect advice that led to penalties.

- Unavoidable absence, such as being in rehab, military deployment, or incarceration.

- Loss of tax records due to circumstances beyond your control, such as theft or destruction.

- Significant financial hardship, where paying taxes on time would have prevented covering basic living expenses.

The IRS generally does not accept ignorance of tax laws, forgetfulness, or lack of funds alone as reasonable cause. However, you may have a case if circumstances beyond your control caused financial hardship.

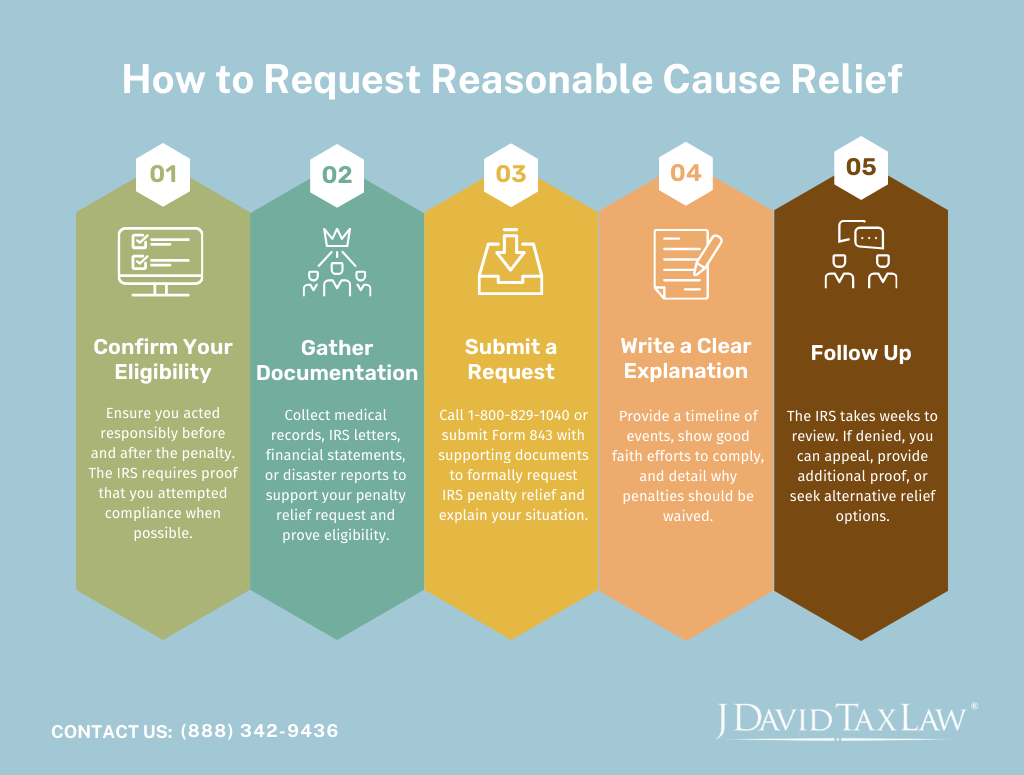

How to Request Reasonable Cause Relief

To apply for Reasonable Cause Penalty Relief, you must provide clear evidence that circumstances beyond your control prevented you from meeting your tax obligations. Follow these steps to submit your request:

- Confirm Your Eligibility – Review the circumstances that led to your IRS penalty. The IRS will want to see that you acted responsibly before and after the event and made efforts to comply when possible.

- Gather Documentation – Collect records that support your claim, such as:

- Medical records, hospital bills, or a doctor’s note for illness-related cases.

- Insurance claims, police reports, or FEMA disaster records for disasters or theft.

- IRS transcripts, letters, or tax law references if IRS misinformation caused the issue.

- Bank statements, foreclosure notices, or other financial documents for hardship claims.

- Submit a Request to the IRS – Call 1-800-829-1040 to explain your situation, or submit Form 843 (Claim for Refund and Request for Abatement) with your supporting documents.

- Write a Clear Explanation – Provide a concise timeline of what happened, when it happened, and how it prevented you from meeting your tax obligations. Show that you acted in good faith and tried to comply as soon as possible.

- Follow Up on Your Request – The IRS typically takes several weeks to review requests. If denied, you have the right to appeal or explore alternative IRS penalty relief options.

The IRS will review your request and supporting documents before making a decision. If approved, your penalties will be waived or reduced. If denied, you can appeal the decision or explore other relief options.

The IRS is Forgiving Millions Each Day. You Could Be Next.

Statutory Exception Relief

Sometimes, taxpayers face penalties due to IRS errors, incorrect guidance, or special provisions in the tax code. You may qualify for Statutory Exception Relief if you were penalized because of misinformation from the IRS or a tax law that provides an exemption.

Who Qualifies for Statutory Exception Relief?

This relief applies when:

- The IRS gave incorrect written advice that led to a penalty.

- A specific tax law exempts you from penalties under certain conditions.

- IRS processing errors caused delays or miscalculations that resulted in penalties.

How to Request Statutory Exception Relief

- Confirm Your Eligibility – Review IRS notices, transcripts, or tax laws to ensure you qualify for relief. If the IRS gave incorrect advice, it must have been provided in writing (not just verbal guidance).

- Gather Documentation – Collect copies of IRS letters, tax transcripts, or official IRS guidance that prove the incorrect advice. If your case is based on a tax law exemption, include references to the relevant statute or IRS ruling.

- Submit a Request for Penalty Removal – Complete Form 843 (Claim for Refund and Request for Abatement) and attach your supporting documents. Clearly state how IRS misinformation or a statutory exemption justifies penalty removal.

- Write a Clear Explanation – Provide a concise, detailed explanation of why the penalty should be removed. Specify the date of the incorrect IRS advice or tax law reference and how it directly caused the penalty.

- Follow Up with the IRS – After submitting your request, check the status by calling 1-800-829-1040. You can appeal the decision or seek further clarification on applicable laws if denied.

Administrative Waivers

In certain cases, the IRS provides penalty relief through Administrative Waivers, which are special exceptions granted for specific circumstances. These waivers are often issued in response to IRS policy changes, processing delays, or large-scale relief programs affecting many taxpayers.

Who Qualifies for Administrative Waivers?

You may be eligible if:

- The IRS has announced a temporary relief program for a specific tax year or group of taxpayers.

- There were IRS processing delays that prevented timely filing or payment.

- The IRS made an error that caused penalties to be misapplied.

One typical example is the First-Time Penalty Abatement (FTA), which falls under administrative waivers and allows penalty removal for eligible taxpayers with a clean filing history.

How to Request an Administrative Waiver

- Verify If Relief Applies to You – Check IRS announcements on IRS.gov or call 1-800-829-1040 to confirm if a waiver is available for your situation.

- Review IRS Notices – If you received a penalty notice, read it carefully to see if the penalty qualifies for an administrative waiver. Some notices will specify if relief is automatically applied or if you need to request it.

- Prepare a Request (If Needed) – If your penalty was not waived automatically, submit Form 843 (Claim for Refund and Request for Abatement) to formally request removal.

- Provide Supporting Documentation – Attach any IRS notices, transcripts, or official announcements showing eligibility. If applicable, include evidence of IRS processing errors or tax law changes that led to the penalty.

- Follow Up with the IRS – If you don’t receive confirmation within 30–60 days, call the IRS to check the status of your request. In some cases, you may need to appeal the decision if the waiver is denied.

Underpayment Penalties (Estimated Tax Penalties)

Underpayment penalties apply when you don’t pay enough tax throughout the year through withholding or estimated quarterly payments. These penalties are common among self-employed taxpayers and anyone with income that isn’t subject to traditional withholding. Unlike other penalties, First-Time Penalty Abatement (FTA) does not apply to estimated tax underpayments—but certain exceptions and IRS errors may still justify penalty removal.

1. What Underpayment Penalties Are

The IRS charges an underpayment penalty when:

- You fail to pay enough tax during the year

- Your withholding is too low

- Your estimated quarterly payments are missed or inaccurate

These penalties are calculated using IRS Form 2210, which determines if your payments were sufficient each quarter.

2. Who Gets These Penalties Most Often

Underpayment penalties typically affect taxpayers whose income is not fully withheld:

- Self-employed individuals and independent contractors

- Gig workers and freelancers

- Investors with capital gains, dividends, or rental income

- Taxpayers with seasonal, uneven, or large end-of-year income events

Even high-income W-2 earners can receive these penalties if bonuses or secondary income are not properly withheld.

3. When Underpayment Penalties Can Be Removed or Reduced

You may qualify for partial or full relief when certain IRS exceptions apply:

- Safe Harbor Rules

You avoid the penalty if you paid at least:- 90% of your current-year tax, or

- 100% of your prior-year tax (110% for high-income taxpayers)

- Uneven Income Exception

If your income fluctuates significantly during the year, the IRS may reduce or waive penalties for quarters where payment timing was reasonable. - Retired or Disabled Taxpayers

If you retired after turning 62 or became disabled during the year, penalties may be reduced. - Disaster or Casualty Events

IRS disaster declarations or unexpected casualty losses can justify penalty reduction.

IRS Miscalculations

The IRS occasionally applies interest rates or penalty periods incorrectly. These errors can be challenged and corrected.

4. When to Use Form 843 to Challenge Underpayment Penalties

If the IRS misapplies Form 2210, calculates the penalty incorrectly, or fails to apply safe harbor or uneven income rules, Form 843 (Claim for Refund and Request for Abatement) can be used to request penalty removal.

Form 843 is also appropriate when:

- Penalties stem from IRS delays or errors

- Interest tied to a miscalculated penalty needs to be removed

- You need a written, formal review of your case

5. Attorney Positioning

- Underpayment penalties cannot be removed using First-Time Penalty Abatement.

- However, they can be challenged through:

- Reasonable cause arguments

- Safe harbor exceptions

- Uneven income calculations

- IRS errors on Form 2210

- Disaster relief provisions

A tax attorney can review your transcripts, verify IRS calculations, apply safe harbor rules correctly, and file a stronger Form 843 request when needed.

Installment Agreements and Penalty Reductions

If you can’t afford to pay your full tax debt upfront, the IRS offers Installment Agreements, which allow you to pay your balance over time. While setting up a payment plan won’t remove penalties entirely, it can reduce failure-to-pay penalties and prevent further enforcement actions, such as tax liens or wage garnishments.

Who Qualifies for an Installment Agreement?

Most taxpayers with outstanding tax debt can negotiate with the IRS and apply for an installment agreement, but approval depends on the following:

- The amount you owe (individuals owing $50,000 or less in tax, penalties, and interest are more likely to qualify).

- Your ability to make monthly payments based on your financial situation.

- Your history of filing tax returns on time (the IRS may require you to file missing returns first).

The Failure-to-Pay Penalty, usually 0.5% of your monthly unpaid taxes, is reduced to 0.25% if you are on a formal installment agreement and making timely payments. If you're unsure how this works, check out our guide on how the IRS calculates interest on tax penalties for a complete breakdown.

How to Request an Installment Agreement

- Determine Your Eligibility – Ensure all required tax returns are filed. The IRS typically won’t approve a payment plan for taxpayers with unfiled returns.

- Choose a Payment Plan – Decide whether you need a short-term (up to 180 days) or long-term (over 180 days) payment plan. Short-term plans don’t require a setup fee, while long-term agreements do.

- Apply Online, by Phone, or by Mail – The easiest way to apply is through the IRS Online Payment Agreement Tool at IRS.gov. You can also call 1-800-829-1040 or submit Form 9465 (Installment Agreement Request) by mail.

- Set Up Monthly Payments – If you owe more than $25,000, the IRS may require automatic direct debit payments. Lower balances may allow manual monthly payments.

- Follow Payment Terms to Avoid Default – Missing payments can lead to penalties resuming at full rates, IRS enforcement actions, or cancellation of your agreement.

Once approved, your penalty rate will be cut in half, and you’ll avoid aggressive collection actions as long as you stick to your payment plan. If your financial situation changes, you may be able to renegotiate your agreement or apply for an alternative relief option.

Offer in Compromise (OIC) for Penalty Relief

If you owe more taxes than you can realistically pay, the IRS may allow you to settle your tax debt—including penalties—for less than the full amount owed through an Offer in Compromise (OIC). This option is designed for taxpayers facing significant financial hardship or those who can prove that paying their full tax bill would be impossible or unfair.

Who Qualifies for an Offer in Compromise?

The IRS approves OICs only when it believes collecting the full amount is unlikely. You may qualify if:

- You cannot afford to pay your total tax debt even through an installment agreement.

- There is doubt as to the accuracy or legitimacy of the tax debt (i.e., the IRS may have assessed the tax incorrectly).

- Forcing full payment would create extreme financial hardship, making it unfair for the IRS to collect the full amount.

When reviewing OIC requests, the IRS considers your income, expenses, asset equity, and ability to pay. You will not qualify for an OIC if you are currently in bankruptcy or have unfiled tax returns.

How to Apply for an Offer in Compromise

- Check Eligibility with the IRS OIC Pre-Qualifier Tool – Before applying, use the IRS Offer in Compromise Pre-Qualifier Tool on IRS.gov to see if you meet the requirements.

- Complete the Application Package – Submit Form 656 (Offer in Compromise) along with Form 433-A (OIC) for individuals or Form 433-B (OIC) for businesses. These forms detail your financial situation and ability to pay.

- Propose a Reasonable Settlement Amount – The IRS will only accept an offer if it reflects the maximum amount they can expect to collect from you, given your financial condition. Lowball offers are usually rejected.

- Pay the Application Fee and Initial Payment – Most applicants must pay a $205 non-refundable fee and include an initial payment with their offer. Low-income taxpayers may qualify for a fee waiver.

- Wait for IRS Review and Decision – The IRS may take several months to review your OIC. During this time, penalties and interest continue to accrue, but IRS collections are usually paused.

If your OIC is approved, you will settle your tax debt for the agreed amount, and any remaining penalties and taxes will be waived. You can appeal the decision within 30 days or explore other penalty relief options, such as an installment agreement if denied.

Because the IRS accepts less than 40% of OIC applications, working with our tax professional can increase your chances of approval.

Which IRS Penalty Relief Option Is Right for You?

Relief Type | Best For | What It Can Remove | Key Requirement |

FTA | First-time issues | Late filing, late payment | 3-year clean history |

Reasonable Cause | Illness, disaster, emergencies | Most penalties | Strong documentation |

Underpayment Relief | Estimated tax issues | Form 2210 penalties | Safe harbor rules |

Statutory Relief | IRS errors or written advice | IRS-caused penalties | IRS letters/proof |

Administrative Waiver | IRS-wide relief events | Bulk penalty removal | IRS announcements |

Installment Agreement | Can't pay in full | Cuts penalty rate | Payment plan approval |

Offer In Compromise | Serious hardship | Tax + penalties | Limited financial ability |

Appeals | Denied requests | Any penalty | File within 30 days |

How to Request IRS Penalty Relief

What to Do If the IRS Denies Your Penalty Relief Request

An IRS denial is not the end of the road. Many taxpayers win penalty relief on a second review—especially when the case is presented with the right documentation and legal argument.

1. Review the Denial Letter

The IRS will explain why your request was rejected.

Common reasons include missing documentation, unfiled returns, or an incomplete explanation.

2. Fix Issues Before Reapplying

Correct anything the IRS flagged, such as filing missing returns or adding stronger supporting documents.

3. Request an Appeal Within 30 Days

You have the right to have your case reviewed by the IRS Independent Office of Appeals, a separate department that often gives taxpayers a fair second look.

4. Present a Stronger Case

Include a timeline, updated evidence, and a clearer explanation of reasonable cause or compliance history.

5. Consider Attorney Representation

Appeals is where legal strategy matters most.

An attorney can identify IRS errors, prepare a stronger case file, and represent you during your Appeals conference.

Attorney Insight

“Most penalty abatement denials happen because taxpayers don’t provide enough detail the first time. A well-documented timeline and a properly framed legal argument can turn a denial into an approval.”

Conclusion

IRS penalties don’t go away independently—they continue to grow over time, worsening your tax situation. The sooner you take action, the better your chances of securing relief and stopping additional charges.

J. David Tax Law has helped thousands of taxpayers successfully reduce or remove IRS penalties, negotiate manageable payment plans, and avoid aggressive IRS enforcement. Contact us today and let our experienced tax attorneys start working on your case immediately.

Looking for More Information?

What Penalties Can Be Removed with IRS First Time Penalty Abatement?

5 Straightforward Ways to Reduce or Eliminate IRS Penalties

Federal back tax abatement program: The Taxpayer’s Guide

Top 5 Reasons the IRS Denies Penalty Abatement Requests

Avoid the IRS Failure to Pay Penalty – 5 Ways to Fix Your Unpaid Taxes Fast

Frequently Asked Questions

To request a penalty waiver, write a formal letter to the IRS explaining why you could not comply, citing reasonable cause such as illness, disaster, or financial hardship. Include supporting documents, reference your tax notice number, and request relief under First-Time Penalty Abatement (FTA) or Reasonable Cause Relief. Read our article for a complete guide on how to get the IRS to waive tax penalties and avoid paying more than you should.

The IRS 6-year rule refers to its authority to audit tax returns up to six years old if it finds a substantial understatement of income (typically 25% or more). This is an extension of the standard 3-year audit period, and there is no statute of limitations in cases of fraud. Keeping detailed tax records for at least six years can help protect against unexpected audits.

Yes. You can request penalty removal through First-Time Abatement, Reasonable Cause, or IRS administrative waivers. When a penalty is removed, the interest connected to that penalty is also removed. However, the IRS does not reduce interest on the tax itself unless the IRS makes an error.

Yes, you may qualify for penalty relief if you have a valid reason for late or missing filings. The IRS may waive the failure to file a W-2 penalty if you can prove reasonable cause, such as a natural disaster, serious illness, or IRS error. First-Time Penalty Abatement (FTA) may also apply if you have a good compliance history.

An IRS civil penalty is a monetary fine for violations like late tax payments, failure to file, underpayment, or inaccurate reporting. These penalties can accumulate with interest and vary based on the type of infraction and the taxpayer’s history. If you’ve been assessed a civil penalty, you may qualify for penalty relief through abatement programs—consulting a tax attorney from J. David Tax Law can help determine the best course of action.

You can avoid tax penalties by filing your return on time, paying your taxes by the deadline, keeping your estimated tax payments accurate, and correcting any missing or late filings quickly. Staying current with all IRS notices and entering a payment plan if you can’t pay in full also prevents additional penalties.