Understanding The Concept of Tax Liens

A federal tax lien is the government’s legal claim against your property when you fail to pay a tax debt. Once the IRS assesses your liability and sends a demand for payment, a lien can be filed if the debt remains unpaid.

This isn’t just a letter from the IRS—it’s a formal action. The IRS records a Notice of Federal Tax Lien (NFTL) in public records, putting your name and debt on file for lenders, employers, and other entities to see.

Unlike a levy, which seizes assets, a lien is a claim. But its presence can stop you from selling, refinancing, or transferring ownership of property. It can also prevent access to credit and affect major financial decisions.

Since April 2018 tax liens are no longer reported on consumer credit reports by major bureaus, but still show up in public records, mortgage applications, and title searches. That visibility alone is enough to stall major life plans, especially involving property.

In short, a lien doesn’t just sit quietly on your file. It can hold your assets hostage until you act to resolve it.

Ways to Remove Tax Liens from Your Property

Removing a federal tax lien isn’t automatic, even after you’ve paid your debt. The IRS has formal processes to release, withdraw, or work around liens, but you must request them and meet specific conditions. Below are the main methods to legally remove tax liens from your property or public record.

1. Paying the Tax Debt in Full

This is the most direct route. Once your full tax balance is paid, the IRS will release the lien within 30 days. A lien release means the IRS no longer has a claim against your property, but the lien may still remain on public record unless you request a withdrawal.

If you’re able to pay in full or through financing, this is typically the fastest way to get the lien removed and restore full control over your property.

2. Requesting a Lien Withdrawal (IRS Form 12277)

A lien release ends the IRS’s claim, but a withdrawal removes the lien from public record altogether. This step is essential if you’re trying to clean up public listings that can affect future financial transactions.

You can apply for a withdrawal if:

-

Your tax debt has been fully paid, and the lien is already released, or

-

You’ve entered into a qualifying Direct Debit Installment Agreement and have a clean compliance history

To apply, submit IRS Form 12277 with documentation showing your eligibility. If approved, the IRS will notify credit bureaus and public record offices. Alternatively, you can book a free consultation with a tax lawyer to see if you qualify for a tax lien release and professional guidance during application.

3. Discharge of Property (IRS Form 14135)

If you need to sell or refinance a property that’s tied up by a lien, you may be able to request a discharge, which removes the lien from that specific asset.

This doesn’t eliminate your tax debt or the lien entirely, but it allows the transaction to go through. You’ll need to show that the IRS will still be able to collect its debt after the sale, or that there’s little or no equity left in the property after senior liens.

To apply, submit the IRS Form 14135 well in advance of the closing.

4. Subordination (IRS Form 14134)

Subordination doesn’t remove the lien, but it reorders the IRS’s claim to allow another creditor, like a mortgage lender, to move ahead. This can make it possible to refinance or qualify for a loan despite the lien.

It’s often used when refinancing could help you pay off the IRS or improve your financial situation. To apply, you must show how subordination benefits both you and the government.

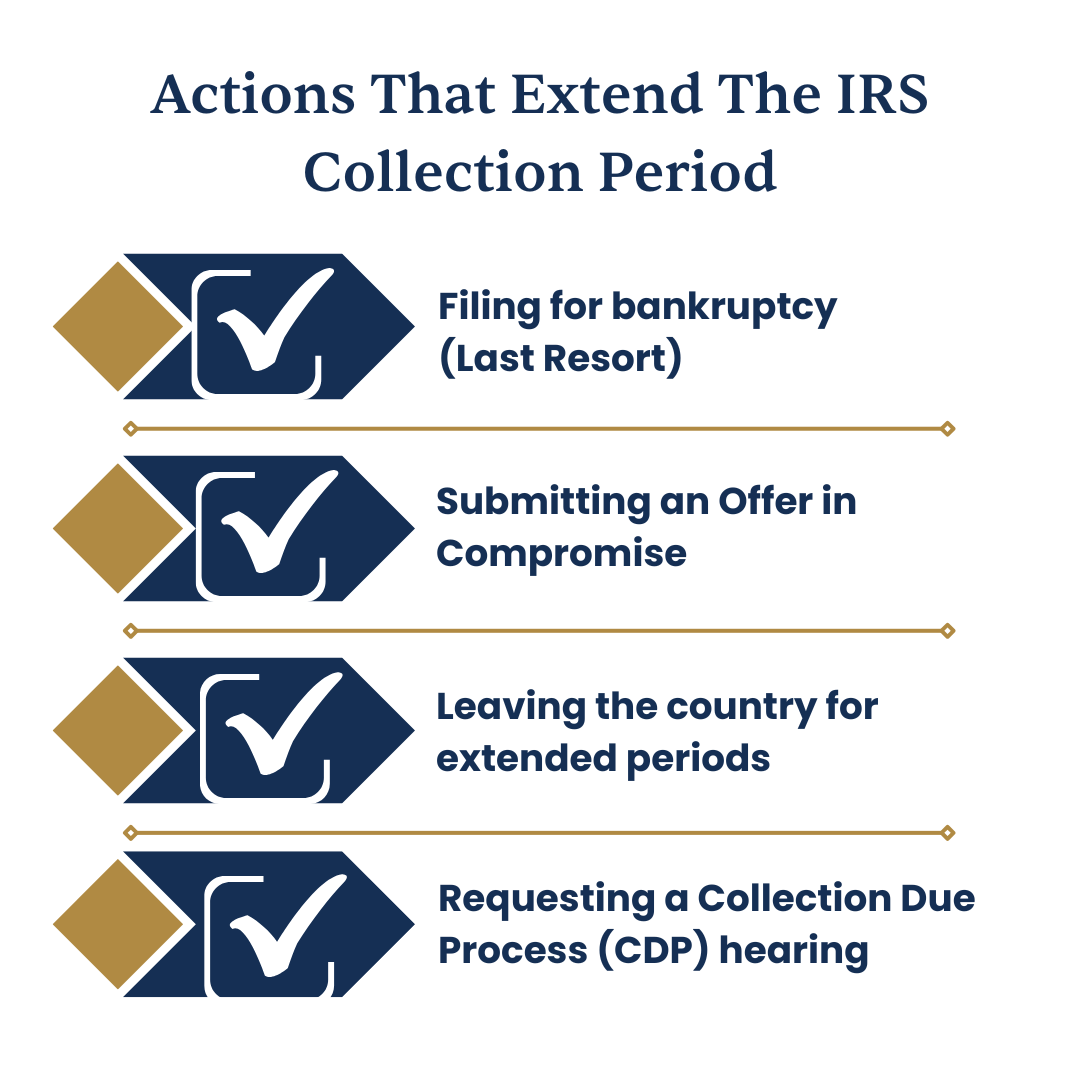

How Long Does a Federal Tax Lien Last?

A federal tax lien typically stays in place until the tax debt is fully paid or becomes legally unenforceable. Under the IRS’s Collection Statute Expiration Date (CSED), the government has 10 years from the date of assessment to collect the debt. Once that window closes, the IRS generally can no longer enforce the lien.

However, the situation isn’t always that simple.

Even after a lien is released, which ends the IRS’s claim, the record of it can remain in public records. That’s why many people also request a lien withdrawal, which removes it from the public record entirely and helps restore financial credibility.

In short, while time is a factor, passively waiting for a lien to expire rarely works in your favor. If the lien is already affecting your property, credit, or financial plans, the better route is to act fast.

How to Get a Tax Lien Removed from Public Record

Even after a tax debt is paid and the IRS releases the lien, the public record remains unless you request an official withdrawal. This distinction matters, especially if you’re applying for a mortgage, loan, or job where financial records are reviewed.

The IRS does not automatically remove a lien from public record when it’s released. Instead, you must submit a formal request using IRS Form 12277 (Application for Withdrawal of Filed Notice of Federal Tax Lien).

You may qualify for a withdrawal if:

-

You’ve fully paid the debt, and the lien has been released

-

You’re in a qualifying Direct Debit Installment Agreement and meet other IRS criteria

-

The lien was filed in error or under unusual circumstances that justify withdrawal

Once approved, the IRS will notify public offices and credit reporting agencies, effectively erasing the lien from searchable records. This can help restore your financial reputation and simplify future transactions involving credit or property.

If you’re unsure whether you qualify or want to avoid delays or denials, it’s smart to have a tax attorney assist with the application and supporting documents.

Get Professional Help to Remove a Tax Lien

A federal tax lien doesn’t just affect your property—it affects your freedom to borrow, refinance, sell, or plan for the future. But the IRS offers structured, legal ways to resolve it. Whether that means paying off the debt, requesting a withdrawal, or applying for discharge or subordination, there are clear paths to relief.

Still, knowing what to do and getting it done are two different things. IRS forms must be filled out correctly. Deadlines matter. And choosing the wrong approach can lead to delays or missed opportunities.

That’s where professional help makes all the difference. A tax attorney can assess your situation, choose the most effective strategy, and handle the paperwork from start to finish, so you don’t have to figure it out alone.

J. David Tax Law has helped countless individuals resolve liens, settle tax debt, and regain control of their financial lives. If you’re ready to remove the lien and move forward, their experienced legal team can guide you every step of the way.