Comprehensive Guide To Dealing With Pennsylvania vs. Federal Tax Debt

If you owe taxes in Pennsylvania, it is important to understand that state and federal tax debt are handled differently . Each has its own rules, collection process, and potential consequences.

The Pennsylvania Department of Revenue often acts faster than the IRS and may involve private collection agencies . State tax debt can escalate quickly if left unresolved.

The IRS manages federal tax debt. While the IRS process is more standardized, it can also result in serious enforcement actions, including liens, levies, and wage garnishments .

If you owe both, these processes run independently. Handling one does not stop the other. This is why a coordinated legal strategy is critical, especially in Pennsylvania.

How State Tax Debt Happens

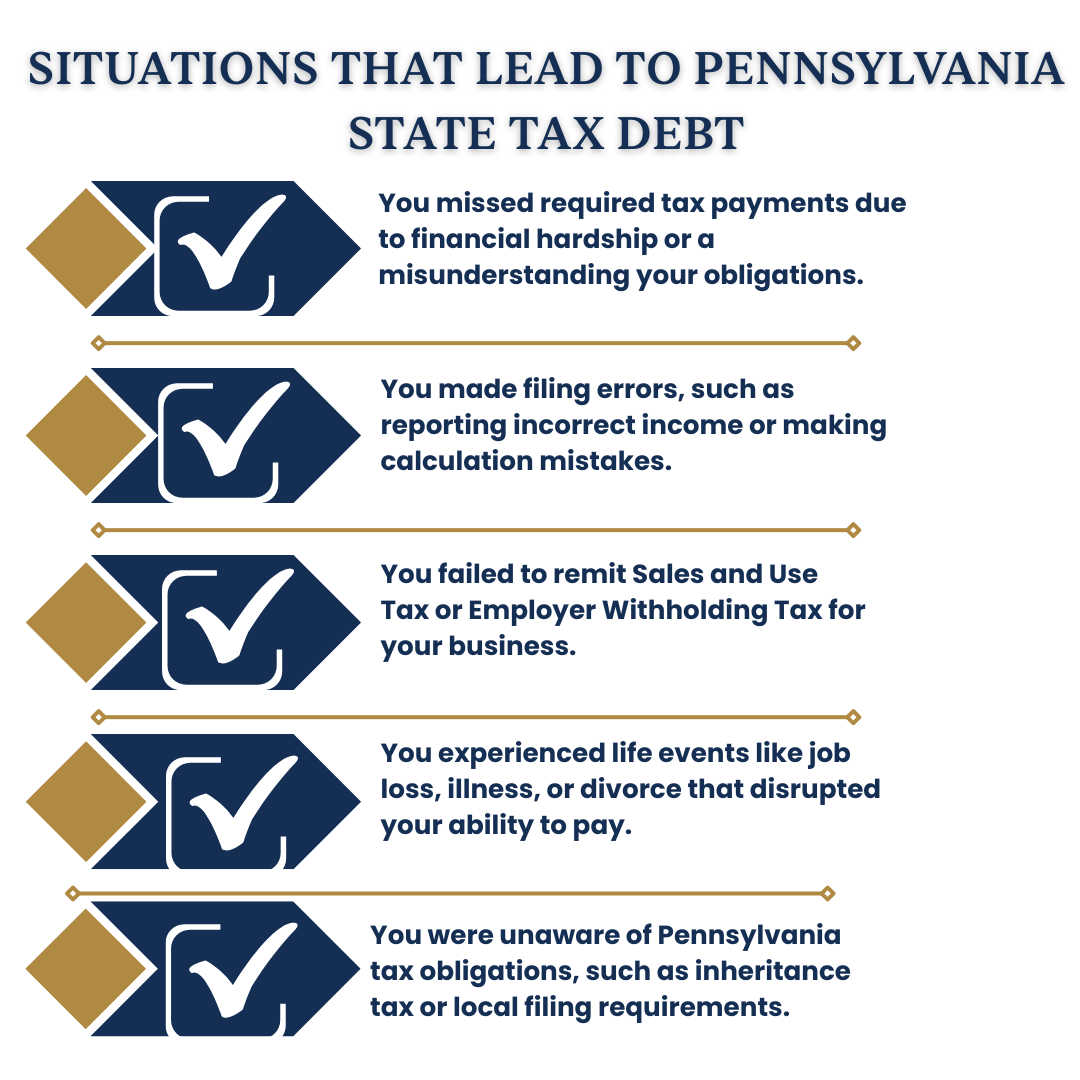

There are many reasons why Pennsylvania residents and business owners fall behind on their state tax obligations. In our experience helping clients resolve both IRS and Pennsylvania state tax debt , the most common causes include:

Comparing Pennsylvania State Tax Debt vs. IRS Tax Debt

Pennsylvania State Tax Debt

Pennsylvania state tax debt arises when required state taxes are not paid to the Pennsylvania Department of Revenue . The most common types include:

Pennsylvania Personal Income Tax

Pennsylvania imposes a flat 3.07% personal income tax on taxable income. Individuals who fail to file or pay this tax on time accrue penalties and interest and may face collection actions from the Department of Revenue.

Sales and Use Tax

Businesses in Pennsylvania must collect and remit a 6% state sales tax on taxable goods and services. It increases up to 8% with local rates if you stay in cities such as Philadelphia. Failing to remit collected sales tax or self-assessed use tax on out-of-state purchases leads to significant penalties. As a result, businesses operating in Philadelphia must comply with both state and local tax rules, adding an extra layer of complexity to tax compliance.

Inheritance Tax

Pennsylvania levies an inheritance tax on transfers of property from deceased persons. Rates vary by the beneficiary’s relationship to the decedent:

-

4.5% for direct descendants (children, grandchildren)

-

12% for siblings

-

15% for other heirs

Failure to file and pay inheritance tax can result in liens and collection actions.

Employer Withholding Tax and Other Business Taxes

Employers are required to withhold Pennsylvania personal income tax from employees’ wages and remit it to the state. Failure to do so leads to liability for the tax, penalties, and potential personal assessment against responsible individuals. Other business-related taxes include gross receipts tax, liquor tax, and cigarette tax.

IRS Tax Debt

IRS tax debt consists of unpaid federal taxes owed to the Internal Revenue Service . Common types include:

Federal Income Tax

Federal income tax is imposed on individuals under a progressive rate structure, currently ranging from 10% to 37% (2024 tax brackets). Taxpayers who fail to pay in full or on time will incur penalties and interest, with the IRS pursuing collection.

Self-Employment Tax

Self-employed individuals must pay 15.3% in self-employment tax, covering Social Security and Medicare contributions. Failure to pay this tax timely leads to significant penalties, especially because no employer is responsible for withholding it.

Trust Fund Recovery Penalty

The IRS assesses a Trust Fund Recovery Penalty against individuals responsible for collecting and remitting payroll taxes (e.g., employee income tax withholding and FICA taxes). If these taxes are not remitted, responsible persons may become personally liable for 100% of the unpaid trust fund taxes.

How Collection Processes Compare: Pennsylvania vs. IRS

State and IRS tax debt collection processes follow different timelines and enforcement methods that every taxpayer should understand. In cities like Philadelphia, local tax compliance adds further risk.

The city enforces its own Business Income & Receipts Tax (BIRT) and Net Profits Tax, which can also trigger local collection actions in addition to state enforcement. Taxpayers often face simultaneous collection efforts from the city, the Pennsylvania Department of Revenue, and the IRS.

Notices and Escalation

Both the Pennsylvania Department of Revenue and the IRS begin collections by sending notices to the taxpayer. However, Pennsylvania’s escalation process typically escalates faster , especially when debts are referred to private collection agencies.

-

The IRS follows a structured process with a series of notices before taking enforced collection actions.

-

Pennsylvania may move to collection after fewer notices, and often involves private agencies that pursue collection more aggressively and on a faster timeline.

Tax Liens

Both agencies can file tax liens against a taxpayer’s property.

-

Pennsylvania files state tax liens with the county prothonotary and the Department of State, which can impact property sales and credit.

-

IRS liens are filed federally and recorded in public records, affecting credit and financial standing.

Wage Garnishment

Pennsylvania can issue a wage garnishment order if a taxpayer fails to respond to notices. According to the Department of Revenue, a 10% wage garnishment is applied to each paycheck until the debt is paid or another resolution is reached.

-

Pennsylvania’s garnishment requires no court approval.

-

IRS wage garnishments, or wage levies , generally follow a formal notice process and typically garnish a portion of wages based on IRS exemption calculations.

Bank Levies

Both agencies have the authority to issue bank levies to seize funds from the taxpayer’s bank accounts.

-

In Pennsylvania, bank levies can be initiated by the Department of Revenue or by private collection agencies working on its behalf.

-

The IRS issues a bank levy only after sending a Final Notice of Intent to Levy and providing the taxpayer an opportunity to request a hearing.

Use of Private Collection Agencies

-

Pennsylvania routinely refers delinquent tax debts to private collection agencies , which are authorized to pursue collections and may engage in frequent phone calls, letters, and even attempts to levy bank accounts or garnish wages.

-

The IRS uses private collection agencies only for older, inactive tax debts, and under a very limited program. Most IRS collections are handled internally.

How Penalties and Interest of Pennsylvania and the IRS Compare

Penalties and interest can add up quickly on both Pennsylvania state tax debt and IRS tax debt, but each agency calculates them differently. On top of that, you also have to consider local tax penalties if you live in a city, like Philadelphia.

Penalty Rates

Pennsylvania Rates

-

Failure to file a quarterly estimated payment : 5% per month, up to a maximum of 25% of the unpaid tax.

-

Failure to file a final return : 5% per month, up to 25% maximum.

-

Additional penalties may apply to specific taxes (such as Sales and Use Tax).

IRS Penalty Rates

-

IRS Failure to file : 5% per month , up to 25% of the unpaid tax.

-

Failure to pay : 0.5% per month , up to 25% .

-

IRS penalties can be reduced or abated for reasonable cause or first-time forgiveness.

Key difference: Pennsylvania’s failure to pay estimated tax penalties is structured similarly to the IRS, but state penalties are often enforced more quickly once debt is assessed.

Interest Calculation

Pennsylvania:

-

Interest on unpaid tax is compounded daily .

-

Rates are adjusted every six months based on the federal short-term rate plus 3% .

-

Current and historical rates are published on the Department of Revenue site.

IRS:

-

Interest is also compounded daily .

-

The IRS uses the federal short-term rate plus 3% , updated quarterly.

-

Interest applies to both tax and penalties.

Key difference: Both agencies apply daily compounded interest at similar rates, but Pennsylvania adjusts its rates biannually and posts them in a slightly different format than the IRS.

How Resolution Options Compare

Both Pennsylvania and the IRS offer resolution options for tax debt, but the scope and formality of these programs differ.

Installment Agreements

Pennsylvania Tax Debt Installment

The Coal State offers payment plans for eligible taxpayers. Terms vary by type of tax and total debt. Personal income tax, for instance, can be installmentally paid in 12 months if it’s below $50,000. Agreements must be requested through the PA Department of Revenue, and interest and penalties continue to accrue. Private collection agencies may also manage payment plans once a case is assigned to them.

IRS Installment Options

The IRS offers short-term and long-term installment agreements. Taxpayers can apply online for debts up to $50,000. Interest and penalties continue to accrue.

J.David Tax Law can help you jump through the legal and administrative loops to work out a favorable payment plan for IRS or state tax debt .

Offer in Compromise (OIC)

Pennsylvania OIC

The Department of Revenue offers an OIC program, but approval is limited to cases of serious hardship or where the tax is uncollectible. PA OIC guidelines emphasize that acceptance is rare and determined on a case-by-case basis.

IRS Offer in Compromise

The IRS OIC program is well-publicized under the Fresh Start initiative . Taxpayers can settle debts for less than the full amount owed if they meet strict eligibility requirements and financial criteria.

Hardship Relief / Currently Not Collectible

Pennsylvania

No formal Currently Not Collectible (CNC) program exists. Temporary hardship relief may be granted at the discretion of the Department of Revenue, typically through negotiation by legal counsel. Taxpayers facing severe financial hardship may request a hold on collection, but this is informal and requires documentation.

IRS

Offers a formal CNC status. Collection actions are suspended for taxpayers who cannot pay after their basic living expenses. Status is reviewed periodically.

Penalty Abatement

Pennsylvania Tax Abatement

Penalty abatement is available for reasonable cause (such as serious illness, natural disaster, or death in the family). Taxpayers must provide supporting documentation, and approval is discretionary.

IRS Tax Abatement

Offers both First-Time Penalty Abatement and reasonable cause abatement. Clear guidelines exist for eligibility. IRS guidance outlines what constitutes reasonable cause, but you may need professional guidance for a successful and/or favorable application.

What to Prioritize if You Owe Both

Pennsylvania collections tend to escalate faster. The state may move to garnish wages or levy bank accounts quickly, especially if your debt is referred to a private collection agency. If you are facing active enforcement from the Pennsylvania Department of Revenue, that typically requires immediate attention.

At the same time, maintaining compliance with the IRS remains important. Ignoring federal notices or failing to address IRS debt can lead to liens and levies that may further compound financial difficulties.

Coordinating your response to both debts is essential . Committing to an aggressive payment schedule with one agency while neglecting the other can trigger new collection actions. It is also important to understand that payment agreements with one agency do not automatically pause collections by the other.

At J. David Tax Law, we help clients evaluate where enforcement risk is greatest and structure payment and resolution strategies that address both debts without causing unintended consequences.

Resolve Your Pennsylvania and IRS Tax Debt With Confidence

Pennsylvania and IRS tax debts are governed by different rules and collection processes. Addressing them requires a clear understanding of each system and a coordinated legal strategy to prevent escalating penalties and enforcement actions.

At J. David Tax Law , our attorneys help clients manage both state and federal tax debt . We understand how quickly Pennsylvania collections can move and how to align resolution strategies with IRS requirements.

If you are facing tax debt in Pennsylvania, with the IRS, or both, we can help you take control of the situation. We are also experts in tax debt resolution for Philadelphia, PA, homeowners and businesses.

Call us today at (888) 342-9436 for a free, confidential consultation.