Did you know the IRS has the authority to revisit your tax filings from past years to assess additional taxes? This guide will clarify how far back the IRS can audit, covering the standard three-year lookback period, the six-year exception for significant income omissions, situations with no time limit for fraud or unfiled returns, the ten-year collection deadline, and essential strategies for defending your position. As dedicated IRS tax attorneys at J. David Tax Law, we are committed to helping clients navigate these complex deadlines, minimize potential risks, and achieve favorable resolutions.

The IRS is Forgiving Millions Each Day. You Could Be Next.

What’s the Standard IRS Audit Statute of Limitations? The 3-Year Audit Lookback Period Explained

The IRS generally has three years from the date your return was filed to conduct an audit and assess additional taxes. This period, known as the statute of limitations for assessment, begins on the original due date of the return or the actual filing date, whichever is later, establishing the timeframe for potential tax adjustments.

Here’s a breakdown of the key audit lookback rules:

| Audit Provision | Revision Window | Applicable Condition |

|---|---|---|

| Standard Statute of Limitations | 3 years | All returns filed on time |

| Substantial Omission Exception | 6 years | Gross income understated by more than 25% |

| No Statute of Limitations | Unlimited | In cases of fraud, willful evasion, or unfiled returns |

Under normal circumstances, most taxpayers will only be subject to reviews within this three-year window, unless specific exceptions apply.

How Does the IRS Define the 3-Year Audit Period?

The three-year audit period is the timeframe during which the IRS is legally permitted to assess additional tax liabilities due to identified discrepancies. This period commences upon the filing of the tax return and concludes precisely three years later, as stipulated by Internal Revenue Code Section 6501. Understanding this timeframe is crucial for effective record-keeping.

To fully grasp this timeline, let’s examine precisely when the clock starts ticking.

When Does the 3-Year Clock Start and Stop?

The three-year period begins on the later of the return’s official due date (typically April 15th) or the date the return was actually filed. If you filed for an extension, the assessment window extends to three years from the extended filing deadline. This ensures the IRS has adequate time to exercise its audit rights.

Now that we’ve established the general timing, let’s consider which types of tax filings fall under this rule.

What Types of Returns Are Covered by the 3-Year Rule?

This rule generally applies to most individual and business tax returns, including Forms 1040, 1120, and 1065, as well as timely filed amended returns. It’s important to note that returns filed late without an extension may result in a shorter lookback period, potentially increasing the risk of review for earlier tax years.

As certain exceptions can extend the IRS’s review period, the following section will address these extended audit timelines.

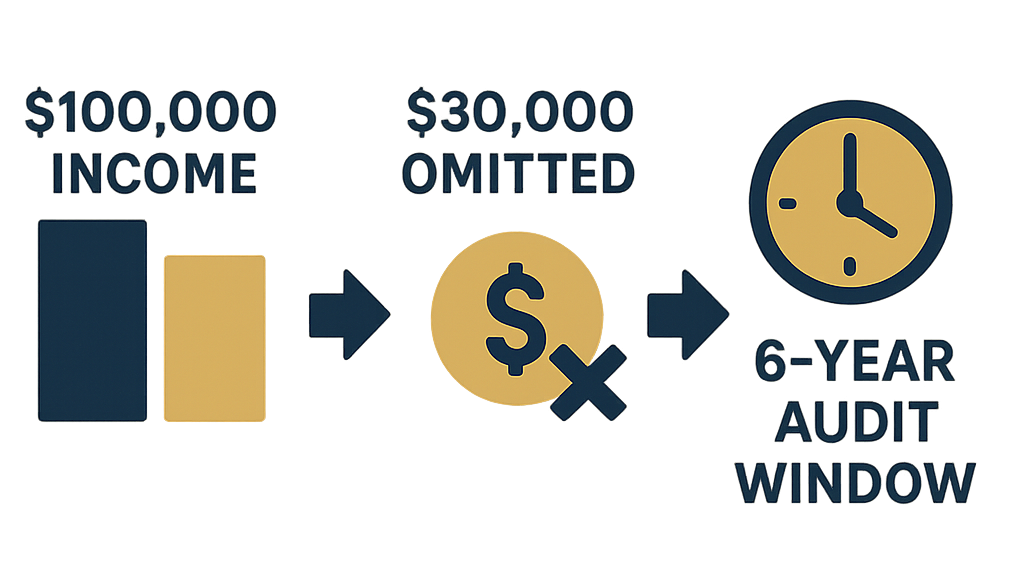

When Can the IRS Audit Beyond 3 Years? Understanding the 6-Year Rule and Substantial Omission

The IRS may extend its audit reach beyond the standard three years, up to six years, if a taxpayer omits more than 25% of their reported gross income. This extended period is designed to address significant underreporting of income.

What Constitutes a Substantial Omission of Income?

A substantial omission is defined as understating your gross income by more than 25%. This could involve failing to report income from sources such as rental properties or significant investment earnings. For instance, if you omit $30,000 in income on a return where your reported income was $100,000, this would trigger the six-year audit window.

Understanding these thresholds for substantial omissions is key to recognizing your extended risk exposure.

| Income Omission Threshold | Audit Window |

|---|---|

| Understatement ≤ 25% | 3 years |

| Understatement > 25% | 6 years |

This structure highlights why accurate income reporting is essential to avoid prolonged IRS scrutiny.

How Does the 6-Year Audit Period Apply to Taxpayers?

If your reported gross income is understated by more than the 25% threshold, the IRS has six years from the original or extended filing deadline to assess additional taxes. This extension is often encountered by high-net-worth individuals and businesses with complex income structures, potentially broadening their audit exposure significantly.

What Are Common Situations Triggering the 6-Year Rule?

Taxpayers may find themselves subject to the six-year audit period in situations involving the omission of income from sources such as:

- Rental properties, royalties, or partnership distributions

- Interest or dividends from foreign bank accounts

- Income derived from informal or underground economic activities

By recognizing these common scenarios, taxpayers can proactively correct their returns and mitigate their audit risk.

Next, we will explore situations where the IRS has no statute of limitations, granting them indefinite authority to audit.

Are There Situations with No Statute of Limitations for IRS Audits? Fraud and Unfiled Returns

In cases involving tax fraud or a deliberate failure to file tax returns, the IRS is not bound by the standard three- or six-year limitations periods. They can audit and assess taxes at any time to address willful evasion.

What Is Tax Fraud and How Does It Affect Audit Time Limits?

Tax fraud is defined as the intentional misrepresentation or concealment of taxable income. When tax fraud is established, the statute of limitations for assessment is removed entirely. For example, claiming fabricated deductions or failing to report income from offshore accounts can expose you to unlimited audit potential and possible criminal prosecution.

How Does Failure to File Tax Returns Impact Audit Lookback?

If you have never filed a required tax return, there is no statute of limitations for the IRS to assess taxes. This means the IRS can pursue taxes for all unfiled years indefinitely. This open-ended exposure underscores the critical importance of timely tax compliance, even if financial resources are limited.

Furthermore, criminal investigations can significantly expand the IRS’s audit rights.

What Are the IRS’s Rights to Audit in Criminal Investigations?

Within the scope of criminal tax investigations, the IRS possesses extensive investigative powers that are not limited by time. This authority, firmly established in federal tax law, allows for a comprehensive examination of documents and financial records that extends beyond typical audit periods to gather necessary evidence.

The following section will clarify how long the IRS has to collect taxes once they have been assessed.

How Long Does the IRS Have to Collect Taxes? Understanding the Collection Statute Expiration Date (CSED)

After taxes have been assessed, the IRS generally has ten years to collect the outstanding amount. This timeframe is known as the Collection Statute Expiration Date (CSED), and it’s important for taxpayers to understand this period for enforced collections.

What Is the Difference Between Assessment and Collection Periods?

The assessment period refers to the IRS’s authority to audit and determine additional tax liabilities. The collection period, on the other hand, is the timeframe allowed for the IRS to actually collect those assessed amounts. These two distinct periods operate sequentially to complete the enforcement process.

Understanding these phases will help us outline specific collection deadlines.

How Long Is the IRS Collection Period After Assessment?

Typically, the IRS has ten years from the date of assessment to collect taxes. After this period expires, the debt generally becomes unenforceable. However, certain actions, such as filing for bankruptcy, entering into an Offer in Compromise, or establishing an installment agreement, can pause or extend this countdown.

Can the Collection Period Be Extended or Suspended?

Taxpayers can influence the collection period by filing for bankruptcy, signing a Form 872 (Consent to Extend the Time to Assess Additional Tax), or entering into installment agreements. Each waiver or suspension impacts the CSED timeline and requires careful legal consideration.

Having reviewed the various deadlines and exceptions, we will now focus on strategic defense measures for audits that extend beyond the standard periods.

What Can Taxpayers Do If Audited Beyond the Standard Period? Legal Defense and Audit Protection Strategies

Responding promptly and strategically to audit notices received outside the standard lookback period is crucial for protecting your rights and limiting your exposure.

How Should You Respond to an IRS Audit Notice Outside the 3-Year Window?

Upon receiving an audit notice, it is essential to immediately verify the date and scope of the notice. Gather all relevant financial records and consult with an IRS tax attorney to discuss challenging any improper assessments. Early intervention can often prevent unwarranted extensions of the audit period.

When Is It Important to Hire a Tax Attorney for Audit Defense?

Engaging a specialized tax attorney early in the audit process provides invaluable strategic guidance, safeguards your procedural rights, and employs effective negotiation tactics to minimize your tax liabilities. Our highly experienced tax attorneys are adept at securing favorable outcomes by presenting compelling evidence and representing your interests before IRS agents.

How Can Waivers and Agreements Affect Audit Timeframes?

Signing a Form 872 or other consent agreements with the IRS can alter audit timeframes, so seeking professional advice is vital to ensure you only agree to terms that align with your best interests. Properly negotiated waivers can effectively balance the need for audit closure with the goal of minimizing your financial exposure.

Transforming audit uncertainty into confidence requires decisive legal support. Contact J. David Tax Law today for a consultation. Discover how our award-winning team and proven track record of success can effectively protect your rights and financial well-being.